"Active" Fleet Will Increase 0.9 Percent By 2030

The FAA's 20 year Aerospace Forecast predicts that the GA

active fleet will grow, but only modestly, over the next 20 years,

and the fleet of piston singles and twins will likely shrink in the

near term before expanding again in the out years of the period.

The category includes forecasts for the fleet and hours flown for

single-engine piston aircraft, multi-engine piston, turboprops,

turbojets, piston and turbine powered rotorcraft, light sport,

experimental and other, such as gliders and lighter than air

vehicles. An "active" aircraft is defined by the FAA as one that

flies at least once per year.

The FAA's 20 year Aerospace Forecast predicts that the GA

active fleet will grow, but only modestly, over the next 20 years,

and the fleet of piston singles and twins will likely shrink in the

near term before expanding again in the out years of the period.

The category includes forecasts for the fleet and hours flown for

single-engine piston aircraft, multi-engine piston, turboprops,

turbojets, piston and turbine powered rotorcraft, light sport,

experimental and other, such as gliders and lighter than air

vehicles. An "active" aircraft is defined by the FAA as one that

flies at least once per year.

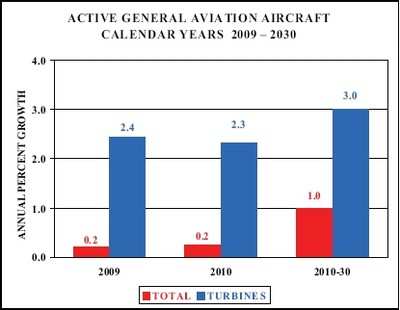

The report indicates that the active general aviation fleet

(chart, below) is projected to increase at an average annual

rate of 0.9 percent over the 21-year forecast period, growing from

an estimated 229,149 in 2009 to 278,723 aircraft by 2030. The more

expensive and sophisticated turbine-powered fleet (including

rotorcraft) is projected to grow at an average of 3.0 percent a

year over the forecast period, with the turbine jet portion

increasing at 4.2 percent a year.

FAA Chart

The number of active piston-powered aircraft (including

rotorcraft) is projected to decrease from the 2008 total of 166,514

through 2017, with declines in both single and multi-engine fixed

wing aircraft, but with the smaller category of piston-powered

rotorcraft growing. Beyond 2017 active piston-powered aircraft are

forecast to increase to 172,613 by 2030. Over the forecast period,

the average annual increase in piston powered aircraft is 0.2

percent. Although piston rotorcraft are projected to increase

rapidly at 3.4 percent a year, they are a relatively small part of

this segment of general aviation aircraft. Single-engine fixed-wing

piston aircraft, which are much more numerous, are projected to

grow at a much slower rate (0.2 percent respectively) while

multi-engine fixed wing piston aircraft are projected to decline

0.8 percent a year. In addition, it is assumed that VLJs and new

light sport aircraft could erode the replacement market for

traditional piston aircraft at the high and low ends of the market

respectively.

Starting in 2005, a new category of aircraft (previously not

included in the FAA’s aircraft registry counts) was created:

“light sport” aircraft. At the end of 2008 a total of

6,811 active aircraft were estimated to be in this category while

the forecast assumes the fleet will increase approximately

825 aircraft per year until 2013. Thereafter the rate of increase

in the fleet tapers considerably to about 335 per year. By 2030 a

total of 16,311 light sport aircraft are projected to be in the

fleet.

The FAA says the advent of a relatively inexpensive twin-engine

very light jet (VLJ) raised a lot of questions regarding the future

impact they may have. The lower acquisition and operating costs of

VLJs were believed to have the potential to revolutionize the

business jet market, particularly by being able to sustain a true

on-demand air-taxi service. While initial forecasts called for over

400 aircraft to be delivered a year, events such as the recession

along with the bankruptcy of Eclipse and DayJet have led the FAA to

temper more recent forecasts.

FAA Chart

The report indicates that the number of general aviation hours

flown (chart, above) is projected to increase by 2.5 percent

yearly over the forecast period. A large portion of this growth

will occur in the short term post recession period, where record

low utilization rates experienced in 2009 will return to normal

trends, particularly in the turbine jet category. As with

previous forecasts, much of the long term increase in hours flown

reflects strong growth in the rotorcraft and turbine jet category.

Hours flown by turbine aircraft (including rotorcraft) are forecast

to increase 4.1 percent yearly over the forecast period, compared

with 1.1 percent for piston-powered aircraft. Jet aircraft are

forecast to account for most of the increase, with hours flown

increasing at an average annual rate of 6.1 percent over the

forecast period. The large increases in jet hours result mainly

from the increasing size of the business jet fleet, along with

measured recovery in utilization rates from recession induced

record lows. Rotorcraft hours, relatively immune to the economic

downturn when compared to other categories, are projected to grow

by 3.0 percent yearly. The light sport aircraft category is

expected to see increases in hours flown on average of 5.9 percent

a year, which is primarily driven by growth in the fleet.

ANN's Daily Aero-Linx (04.15.24)

ANN's Daily Aero-Linx (04.15.24)